Three Lines Model and an Integrated GRC Model

Organizations are operating in an environment where uncertainty, complexity, stakeholder scrutiny, regulatory expectations, cyber threats, geopolitical instability, sustainability pressures, and digital transformation are all accelerating simultaneously. In this environment, governance, risk, and compliance (GRC) can no longer operate as fragmented disciplines. Instead, organizations require an integrated GRC model that aligns governance, risk management, compliance, performance management, assurance, and strategic execution around mission-critical objectives.

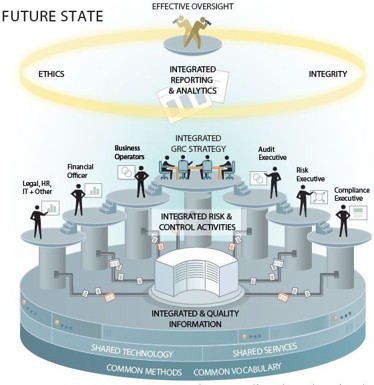

One of the most important frameworks supporting this alignment is the Three Lines Model developed by the “Institute of Internal Auditors”. While the Three Lines Model is often associated primarily with internal audit, its true value lies in its ability to define roles, accountability, and collaboration across the entire organization. When integrated into a broader GRC model, the Three Lines Model becomes a powerful mechanism for ensuring that the board, executive management, operational teams, risk functions, compliance functions, and assurance providers all work together toward the achievement of strategic and mission-critical objectives.

At its core, an integrated GRC model is designed to ensure that organizations can create value, preserve value, and prevent value destruction. It seeks to break down silos between governance, risk management, compliance, internal audit, legal, cybersecurity, ESG, finance, quality, and operational functions. Rather than each function working independently, integrated GRC creates a common language, common objectives, common reporting structures, and a common understanding of risk and performance.

The Three Lines Model provides the structure through which this integration can occur.

The first line consists of operational management and business process owners. These are the people responsible for delivering products, services, projects, revenue, operational efficiency, customer satisfaction, and other key business outcomes. They own risks directly because they own the activities that create risk. The first line is therefore responsible for identifying risks, implementing controls, monitoring performance, managing incidents, and ensuring that mission-critical objectives can be achieved.

The second line consists of functions that support, monitor, advise, challenge, and guide the first line. These typically include enterprise risk management, compliance, legal, information security, health and safety, ESG, finance, quality assurance, and other oversight functions. Their role is not to take ownership of operational risks away from the first line, but rather to establish frameworks, policies, methodologies, reporting structures, and monitoring mechanisms that help the first line operate effectively.

The third line is internal audit, which provides independent assurance over governance, risk management, and control effectiveness. Internal audit evaluates whether the first and second lines are functioning as intended and whether the organization is adequately managing risks that may prevent it from achieving its objectives.

Mission Critical Objectives

The relationship between the Three Lines Model and an integrated GRC model becomes especially important when viewed through the lens of mission-critical objectives.

Mission-critical objectives are the outcomes that are essential for organizational success, survival, sustainability, and stakeholder confidence. These may include maintaining operational continuity, achieving financial targets, protecting customer trust, complying with regulatory requirements, safeguarding cyber infrastructure, achieving ESG commitments, ensuring safety, maintaining asset integrity, or delivering strategic projects on time and within budget.

Too often, organizations manage risks in isolation from strategy. Risk registers become disconnected from business performance, compliance becomes a checklist exercise, and assurance activities focus on controls without understanding whether those controls are protecting the organization’s most important objectives.

An integrated GRC model prevents this disconnect by ensuring that all governance, risk, compliance, and assurance activities are aligned directly to mission-critical objectives.

The board plays a central role in this process. The board is responsible for defining strategic direction, setting risk appetite, approving major policies, ensuring ethical leadership, and overseeing whether management is achieving mission-critical objectives. The board should not merely receive reports on isolated risks or control failures. Instead, it should receive integrated information showing how risks, controls, assurance activities, performance indicators, compliance obligations, and strategic initiatives all interact.

For example, if a board identifies cybersecurity resilience as a mission-critical objective, the integrated GRC model should ensure that:

- The first line owns cybersecurity controls, operational resilience, user behavior, and incident response.

- The second line defines cybersecurity policies, monitoring standards, risk assessments, and compliance requirements.

- The third line provides assurance on whether cybersecurity governance, controls, incident management, and resilience plans are effective.

- Executive reporting shows the relationship between cyber risks, operational performance, regulatory compliance, customer trust, and financial impact.

This same logic applies to other strategic objectives such as ESG performance, supply chain resilience, digital transformation, project execution, fraud prevention, regulatory compliance, and workforce capability.

C-suite Executives

The alignment of C-suite role players is critical within this model.

- The Chief Executive Officer is responsible for ensuring that the entire organization remains aligned to mission-critical objectives and that the culture supports accountability, transparency, performance, and ethical behavior.

- The Chief Financial Officer plays a central role in linking risk, performance, capital allocation, financial resilience, and strategic decision-making. The CFO ensures that risks are considered when resources are allocated and that risk-adjusted performance becomes part of executive discussions.

- The Chief Risk Officer is responsible for establishing the enterprise-wide risk framework, risk appetite methodology, risk reporting processes, and risk escalation mechanisms. The CRO helps ensure that strategic, operational, financial, cyber, ESG, and compliance risks are integrated into decision-making.

- The Chief Compliance Officer ensures that legal, regulatory, and ethical obligations are embedded into business processes and that compliance risks are proactively monitored.

- The Chief Information Officer and Chief Information Security Officer play essential roles in ensuring that digital transformation, cybersecurity, data privacy, and technology resilience are aligned to organizational objectives.

- The Chief Human Resources Officer contributes by ensuring that workforce capability, succession planning, ethics, culture, incentives, and leadership behavior support the organization’s risk and governance objectives.

- The Chief Audit Executive provides independent assurance to the board and audit committee, helping them understand whether governance, risk management, and internal controls are functioning effectively.

An integrated GRC model is therefore not about creating more bureaucracy. It is about ensuring that the board, executive management, and assurance functions all focus on the same mission-critical priorities.

When organizations fail in this area, it is often because functions operate in silos. Risk teams focus only on risk registers. Compliance teams focus only on regulations. Finance focuses only on budgets. Internal audit focuses only on controls. Operations focus only on delivery. The result is fragmented reporting, duplicated effort, inconsistent priorities, and blind spots around mission-critical objectives.

By contrast, organizations with mature integrated GRC models use the Three Lines Model to create clarity of accountability, consistency of reporting, and alignment of priorities. They build dashboards that connect objectives, risks, controls, incidents, compliance obligations, assurance findings, and performance metrics. They ensure that executive committees and boards receive integrated information that supports better decision-making.

Ultimately, the relationship between the Three Lines Model and an integrated GRC model is one of structure and purpose. The Three Lines Model defines who does what. Integrated GRC defines how everyone works together. Together, they create an enterprise-wide system that enables organizations to protect value, create value, and achieve mission-critical objectives with confidence.